This particular topic is a tricky one for me. Depending on the time of day or day of the week, my feelings about this issue constantly changes…and so far, this is what I’ve come up:

If your student loan interest rates are high (>4%), focus on paying down huge chunks of it until you can consolidate/refinance to a lower interest rate.

The reason why I personally think a 4% interest rate is high is because for individuals in our very fortunate situation (meaning our income), there’s no reason why you can’t get a lower interest rate on your student loans. Honestly, I would probably go a step further and say you should be able to get an interest rate lower than 3%. In fact, as I’m writing this, I think I may consider refinancing to get my current rate of ~3.5% to <3%.

In any case, if you’re unable to consolidate/refinance your loans due to a lower than expected credit score (<750), then you ought to focus on paying large chunks of your loan balance until you can rehabilitate your score to get a low interest rate.

If your student loan interest rates are low (<4%) and you have great credit, you can do 1 of 2 things:

- Focus on paying off your student loans by making gargantuan payments with whatever savings you having so that you can shorten the amount of time and ultimately, the interest that you’re paying on your loans…or…

- Make the minimum monthly payment on your loan since the interest you’re paying on those loans are slightly above inflation rates and whatever savings you have, well, pocket it that and find an investment that can get you a better annual return, whether it’s index funds, real estate, your friend’s ridiculous new million dollar idea.

I think from a mathematically viewpoint, option 2 is probably the choice to take, but alas, personal finance decisions aren’t made purely from a rational, mathematical standpoint, is it?

PAYING LOANS OFF FIRST!

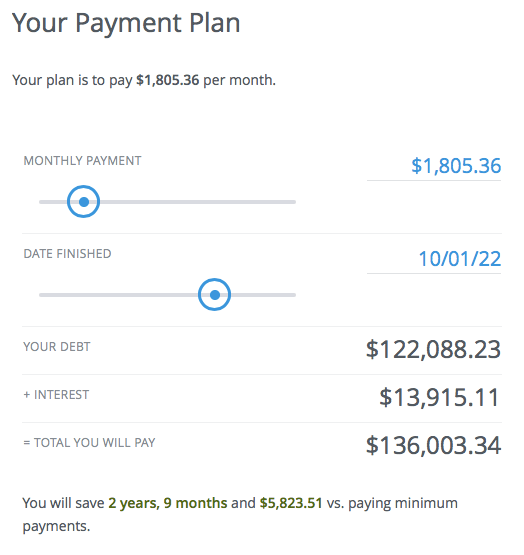

Let’s explore option 1. I’ll use my student loan profile as an example.

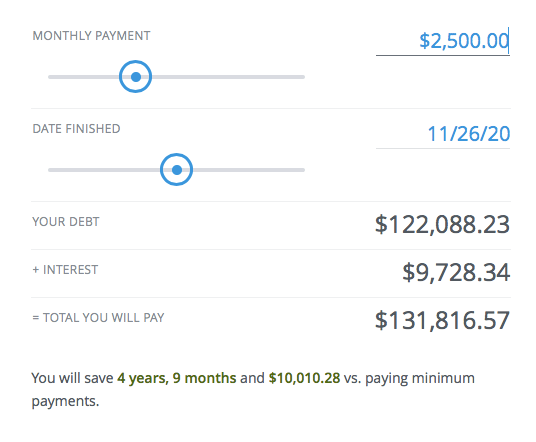

So, after what’s ostensibly 6 years of paying my loans, I’ll have paid ~$14,000 in interest. Let’s see what happens if I increase my monthly payments from $1,800 to $2,500, which I can easily afford giving that I have an approximate monthly savings of $2,900.

- Source: ReadyForZero

By increasing my monthly payments by $700, it looks like I’ll be saving ~$4,000 in interest, which doesn’t really seem all that significant to me given that you can basically make $1,000 with two days of work after taxes. Kind of hard for me to justify not having that extra cash flow. Now, what happens if I add my entire monthly savings ($2900) to with my already allotted $1800 monthly payment to my student loans?

- Source: ReadyForZero

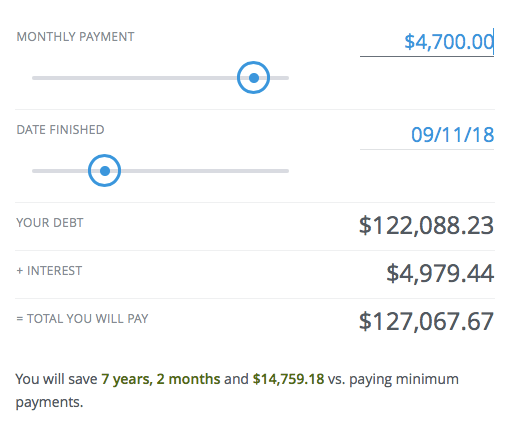

So, comparing this with my original $1800 monthly payments, I’ll be saving $10,000 in interest payments. That’s a pretty sizable lump of change, but is it enough to make me go 2 years without having a savings fund?

And this is where this pursuit becomes more psychological than mathematical.

SAVING $ WHILE MAKING MINIMUM LOAN PAYMENTS

So, let’s say I stay the course with my $1800 monthly payments. We know that by October 2022, which is when I’m slated to pay off my student loans, I’ll have paid ~$14,000 in interest.

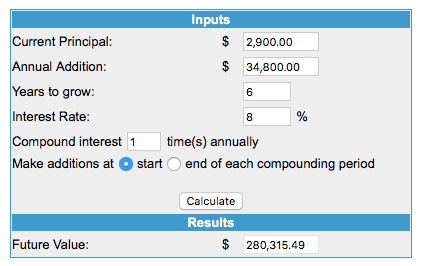

Well, what about the savings I made? Assuming I don’t touch my monthly savings of $2900 and I consistently save this amount over 6 years, this is what I should theoretically obtain:

- Source: MoneyChimp

If I’m saving $34,800 over 6 years, I’ll have saved $208,800 of my own money after taxes. Assuming I’m investing this money into an index fund that returns 8%, I’ll have made ~$71,000 in equity, which isn’t too shabby.

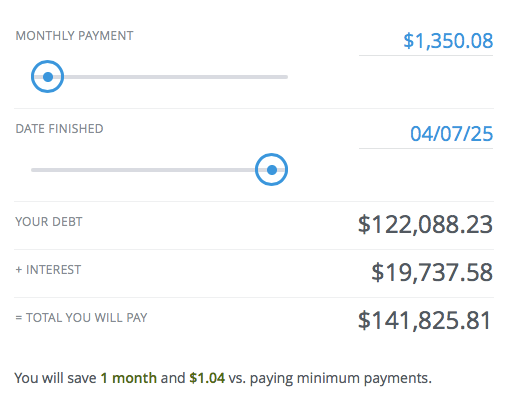

Let’s used another example. Instead of paying $1800, let’s say I revert to making just the minimum payments.

- Source: ReadyForZero

As you can see, my minimum monthly payment of $1350 means it would take me nearly 9 years to pay off my balance and I’ll have paid ~$20,000 in interest payments.

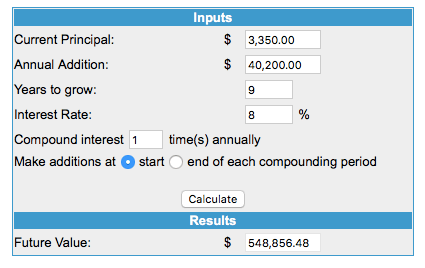

Now, let’s assume that I invest my monthly savings ($2900) + the difference from my original monthly payment with my minimum monthly payment ($1800-$1350=$450). So, on a monthly basis, I have access to $3350. Let’s just say I consistently save $3350 every month for the next 9 years, this is what we’ll see:

- Source: MoneyChimp

Ultimately, while the math seems to be favor option 2, clearly a psychological/emotional component is involved when trying to decide between the two. This is where I have a lot of internal conflict as there are days when I just want to be done with making monthly student payments and the thought of forking over $1800 a month for 6 years sometimes feels like an eternity (never mind the 30 year payment plan some of my colleagues seem to be on, which I personally think is crazy). And as a result, I end up wondering if I should just sacrifice the next 2 years of my life and go gung ho with $4700 in monthly payments so I can be done with it even at the expense of losing equity and cash in hand.

I suppose the answer to this really depends on what you’re comfortable with.